Trade Report #1 - AI Portfolio Allocations for Q4 2023

Trade Report #1 - AI Portfolio Allocations for Q4 2023

Chips ahoy

Welcome to the inaugural e/alpha Trade Report. Below, I’ll walk through the initial allocation of my $10,000 portfolio. Full Trade Reports go out every quarter, and are reviewed the following quarter in a corresponding Investment Review.

This initial report will perhaps be my easiest — in the early stages of the AI boom there is an obvious foundational resource, analogous to the “oil” or “steel” of previous industrial booms, a prerequisite and forerunner of any further economic impact of AI, and a resource with huge moats and high margins.

GPUs

Before I go into the longer-term second, third, and fourth order implications of AI over the coming quarters, I will first build a base portfolio out of the current winners. I’m a bit late to the game, to be honest, but not that late — it’s, say, the top of the 2nd, but the market has clearly priced in a some portion of NVDA’s future value capture from AI — it’s a trillion dollar company with +100 P/E ratio at its latest earnings! The reality, though, is that any GPU supplier has massive headroom for growth — keep in mind a lower bound of matching human cognitive output with GPUs — and this is reflected even in the near term: NVDA’s forward P/E is a more reasonable 30.

It’s easy to get lost in the weeds of specific technologies, near-term capacity constraints, and individual company strategies. The reality is that, when there are hundreds of billions of dollars on the line, the market has a way of solving these issues, and commoditizing things, more quickly and effectively than we usually guess. We need to keep a high-level, big-picture view of where this is headed: huge, sustained growth in GPU flop demand as we switch from human cognition to machine cognition.

So, this round of allocation will go to companies with obvious demand for their current or near-term offerings with regards to current state-of-the-art (SOTA) AI models. I am focusing on companies with leveraged exposure to AI growth, who aren’t experiencing cannibalization.

Considerations

Overall, AI chip suppliers are no-brainer winners in the AI boom. They are very complex, capex-heavy industries that are not easy to compete in. That said, AI chips are currently a small part of most of chip companies’ businesses. There has been a general downturn in the chip demand, as part of a post-covid hangover of over-consumption. Contributing to this some, and more recently offsetting it, has been a pull-forward of demand by Chinese firms looking to get everything in before export controls hit. So, for most firms, there are swirling forces at work — expect turbulence before the big swell of AI lifts all.

Trades

AMD - BUY to 25% allocation

AMD will be shipping their MI300X in 2024, the only chip on the market competitive with Nvidia’s offerings at the top end (Google will have competitive chips, but they are not really available on the market generally). There will be volume constraints, and the initial impact on AMD’s revenues will be small, but cloud buyers should be eager for something to wean their dependence on Nvidia, and we should expect future commitments from those buyers for AMD’s offerings. AMD stock piggybacked on some of the initial NVDA hype but has fallen off since (as their other chip lines have faced headwinds). This is a clear buy.

NVDA - BUY to 25% allocation

The undisputed king of the current AI boom. The majority of generative AI flops are on Nvidia GPUs currently. This has already been priced into their stock, but we should expect Nvidia to continue to lead the industry as AI grows in scope and capability. Threats to their CUDA software moat will begin to grow — too much money is on the other side of that moat for it to be truly defensible — but they still have a big lead in design and the largest revenue base to amortize over. NVDA’s dominance, and unmatched margins, are safe, if only for now — 90% margins can’t last forever in business presumably!

TSM - 0% allocation

AI revenues make up a small fraction of TSM’s total $70B revenue, and will likely result in some cannibalization as big tech focuses on AI build out over other datacenter resources and as actually end jobs migrate from deterministic software to LLM workloads. Although they have a near monopoly on the processes necessary for SOTA GPUs, they have been unable to extract a larger share of NVDA’s margins. I will continue to monitor TSM, and its precarious position on an island that is the flash point of the great power struggle of the 21st century. But for this near-term focused initial allocation, it’s not the right fit.

GOOG - 0% allocation

Alphabet is the third company with competitive $/flop chips for LLM workloads. In fact, their latest generation of TPUs are likely the most cost effective of any available. They lead the industry in total talent, despite losing some notable names, and are the birthplace of the entire AI revolution itself. But in terms of an investable asset, GOOG suffers from a few big problems: 1) Their chips aren’t really for sale 2) their business is already massive — it takes a lot to move the stock 3) their entire generative AI endeavor is on the negative side of the balance sheet for the foreseeable future, and 2) when and if they do productize their AI it is just as likely to cannibalize their primary revenue stream as add to it! I am bullish on GOOG long-term as a potential leader in the space, the only current player with research talent, consumer distribution, massive proprietary data sources, and competitive hardware. But, like TSM, for this near-term focused initial allocation, GOOG is not the right fit.

INTC - 0% allocation

It’s no secret that Intel has fumbled their lead in chips, missing both the mobile revolution and now the AI revolution. They, themselves, are certainly aware of this and working hard to catch back up. As a long-term investment, I’m bullish. For now, I will sit this one out, as I expect I’ll get more out of my capital elsewhere.

ASML - BUY to 20% allocation

ASML is an essential supplier to the SOTA GPU supply chain, and their growth and expectations show it.

CAMT - BUY to 15% allocation

Camtek is a leader in process control with high exposure to the advanced packaging required for SOTA GPUs. This is a more levered, mid-cap bet on AI chips.

FN - BUY to 15% allocation

Another mid-cap play, Fabrinet makes essential optical networking devices for NVDA. It does most of its business in Telecoms currently but that will quickly change as GPUs ramp.

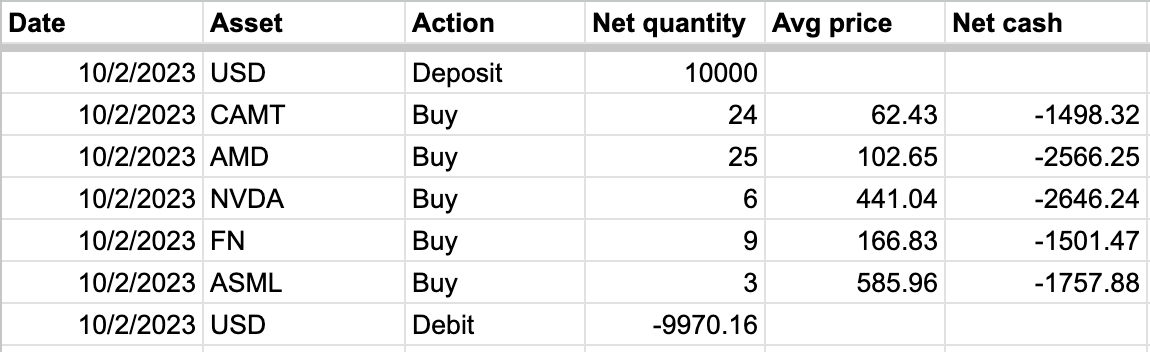

The final tally after actual trades: